How to Buy Before You Sell in Omaha: Bridge Loans, HELOCs & Contingent Offers

You've found the house. Maybe it's in Elkhorn, maybe it's a bigger yard out in Papillion, maybe it's the ranch in Bennington you've been watching for months. There's just one problem: your equity is sitting inside the home you haven't sold yet. So now what?

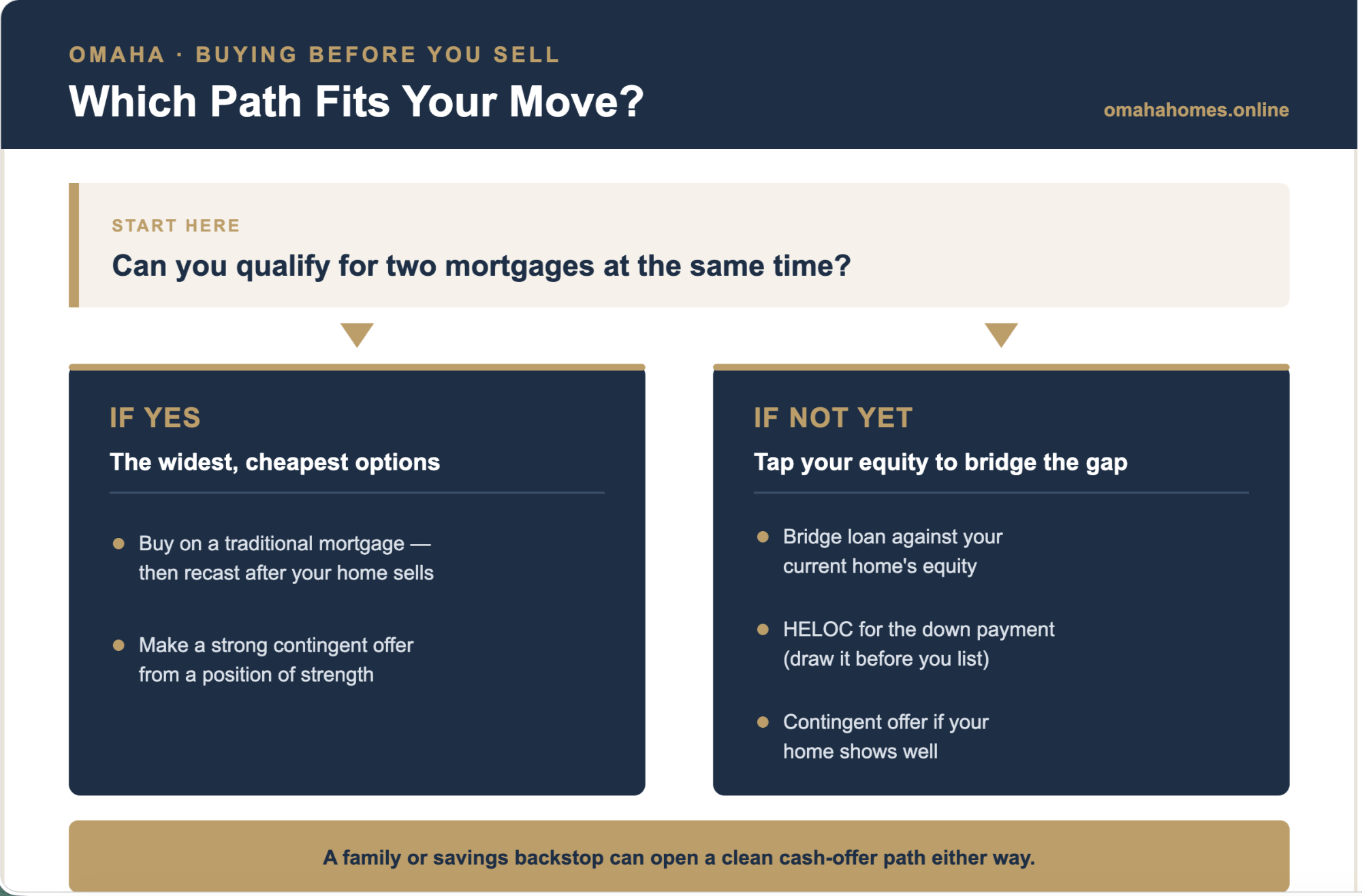

This is the central puzzle for move-up buyers in Omaha, and it doesn't have one universal answer. Bridge loan, HELOC, contingent offer — each one solves the timing gap differently, and each one breaks under different conditions. I've helped clients work through all three paths, and the right one almost always comes down to the same two questions I ask first: Can you qualify for two mortgages at the same time? And do you have a financial backstop — a family member, a savings cushion — if things don't go perfectly?

Your answers tell me more than any rate sheet will. Let's walk through each option so you know what you're actually choosing between.

For the big picture strategy on timing your move, see this guide on buying and selling at the same time.

What This Post Covers

A side-by-side comparison of the three main financing paths for Omaha move-up buyers who need to buy before they sell — including when each one works, when it doesn't, and what I actually recommend first.

The Quick Comparison

Here's the landscape at a glance. We'll go deeper on each option below.

| Option | How It Works | Best For | Typical Cost | Biggest Risk |

|---|---|---|---|---|

| Bridge Loan | Short-term loan (6–12 mo.) secured by your current home's equity; interest-only until you sell | Buyers who need the equity from their current home to close — and their current home is ready to list | 8.5–11.5% APR in today's market; plus origination fees typically 1.5–2.5 points | Carrying two loans if your home doesn't sell quickly; rate is high |

| HELOC | Revolving credit line against your current home's equity; typically used to cover the down payment on the new home while still qualifying for two mortgages | Buyers who can qualify for two mortgages but need to access equity for the down payment; also works well for significant downsizers | Variable, currently ~7.5–10% in Nebraska; lower than bridge loans | Lender can freeze the line once your home goes on the market — funds must be drawn before you list |

| Contingent Offer | Your purchase offer is contingent on your current home selling first; seller takes on your timing risk | Buyers in price ranges where sellers have been sitting on the market; slower-moving neighborhoods | No financing cost; may accept a lower price or include a kick-out clause | Seller can accept a better offer and kick you out; competitive homes won't take it |

Bridge Loans: Fast, Expensive, and Very Specific

A bridge loan is exactly what the name implies — a temporary span between where you are and where you're going. You borrow against the equity in your current home, use those funds toward the purchase of your next one, and pay the loan off when your current home sells. Terms are typically six to twelve months, payments are interest-only, and the rate runs meaningfully higher than a standard mortgage — figure 8.5–11.5% APR in the current environment, plus origination fees that typically run 1.5 to 2.5 points.

That sounds expensive, and it is. But the math often works out when the alternative is losing a house you really want.

I had a client who wanted to buy a condo — cash offer, because the seller wasn't going to entertain a home sale contingency. Her equity was locked in her current home, so we got her qualified for a bridge loan to make it happen. As it turned out, her existing home sold faster than expected, and we were able to convert the deal to a straight cash purchase before we even needed to draw on the bridge. She got the condo, the seller got a clean deal, and the bridge loan did its job just by existing — we never had to fully lean on it.

"Sometimes a bridge loan is less about the money and more about the credibility. It tells a seller you're not guessing — you have a plan."

To qualify, you generally need a credit score of 700 or better, meaningful equity in your current home (most lenders want at least 20% after the bridge is factored in), and a current home that's genuinely ready to list. Two Omaha-area lenders that explicitly offer bridge financing are ACCESSbank (locally owned, straightforward about their bridge product) and Nebraska Bank of Commerce (NBC Bank). These aren't endorsements — shop rates and terms — but they're good starting points if your current lender doesn't have a bridge program.

Where bridge loans break: if your current home sits longer than expected, you're carrying two sets of housing costs at a high rate. The clock is always running. Don't go this route unless your home is priced right and genuinely ready to move.

HELOCs: A Down Payment Tool, Not a Full Replacement

A lot of national content frames HELOCs as a standalone "buy before you sell" solution — as if you'd use one to purchase your next home outright. In Omaha, that's rarely how it works in practice. The more realistic scenario is this: you open a HELOC against your current home's equity, use it to fund your down payment on the new home, and then qualify for a mortgage on both properties at the same time. The HELOC covers the gap in timing; a traditional mortgage does the heavy lifting on the actual purchase.

Current HELOC rates in Nebraska are running roughly 7.5–10% depending on the lender and your credit profile — meaningfully cheaper than a bridge loan — and the interest-only draw period gives you flexibility on cash flow. When the current home sells, you pay off the HELOC balance with the proceeds and you're done. Local credit unions like Centris FCU and Metro Credit Union are worth checking alongside the bigger banks; their rates have been competitive for members.

There is one important catch that most articles skip: many lenders will freeze your HELOC — or block new draws entirely — once your home goes on the market. Their logic is straightforward: a home for sale is a home whose value is in flux. If you plan to use a HELOC for your down payment, you need to draw those funds before you list. Talk to your lender explicitly about this timeline before you count on the money being there.

The other place HELOCs work particularly well is a significant downsize. If you have a paid-off or nearly paid-off home and you're buying at a much lower price point, the HELOC might cover the entire purchase — no second mortgage needed. I've helped clients use this approach to buy investment properties for cash before selling a primary residence, and it's a clean path when the numbers support it. Using a HELOC to stretch into a full move-up purchase at the same price level is a harder equation, but as a down payment tool layered on top of qualifying for two loans, it's one of the more practical options in the toolkit.

The key qualifier throughout: you need to be able to carry both mortgage payments on your income. Use the mortgage calculator to stress-test what that looks like before you open the line.

Want to Explore a HELOC?

If the HELOC route fits your situation, my lending partner Erin Trescott (Senior Loan Officer, Guild Mortgage, NMLS #457124) offers a HELOC you can apply for online. It's a quick way to see what you'd qualify for before you start planning your move — and a good first call if you want someone to walk you through the draw-before-you-list timing.

Start Your HELOC Application →Contingent Offers: Underrated in Today's Omaha Market

A contingent offer simply means: "I want to buy your home, but my ability to close depends on my current home selling first." Two years ago, in the frenzy of the Omaha market, most sellers wouldn't touch one. Today, the picture has shifted.

Inventory across Douglas, Sarpy, and Pottawattamie counties has grown meaningfully heading into 2026 — up over 13% year over year. Homes are averaging around 25–30 days on market, and while desirable homes still move quickly, the intense same-day decision pressure has softened considerably. And here's the thing about days on market: sellers start sweating as those numbers climb. A home that's been sitting for three or four weeks with no offer is a seller who's going to be a lot more open to a conversation that wasn't possible a month earlier.

"Sellers start sweating as the days on market pile up. That's when a contingent offer that would have been laughed at in 2022 suddenly looks pretty good to everyone."

The contingent offer does come with tradeoffs. Sellers in Omaha will typically ask for a kick-out clause — meaning they can continue to market the home, and if a better offer comes in, they give you 48–72 hours to remove your contingency or walk away. You should go in with eyes open about that. You may also give up some negotiating leverage in exchange for the seller absorbing your timing risk.

Where contingent offers tend to work in Omaha right now: homes priced above $400K that have been on the market for a couple of weeks or more. Below that threshold, unless a listing has genuinely been sitting, most sellers aren't going to wait on your home sale when they expect clean offers to come along. In the sub-$400K range the market still moves fast enough that a contingency feels like unnecessary risk to most sellers.

On higher-priced homes, the dynamic is a little different — and there's an important nuance. When a listing agent receives a contingent offer on a $500K or $600K home, the first question they're going to ask their seller isn't just "do we like this buyer's price?" It's "how easy is their home going to be to sell?" If your current home is priced right, shows well, and is in a market that moves, that's a real selling point for the contingency conversation. If it's overpriced or in a tough spot, a savvy listing agent is going to advise their seller accordingly. Come to the table with a realistic picture of your own home's marketability — it matters.

Check out the Spring 2026 Omaha market update for a current read on inventory levels by area — and get a free evaluation on your current home so you know exactly what story you're telling to a prospective seller.

Free Download

Free Omaha Home Buyer's Guide

A practical roadmap through every stage of buying — from pre-approval to closing — with local Omaha tips you won't find anywhere else.

Download Free →Other Paths Worth Knowing

The three headline options get most of the attention, but in practice, I've helped clients work through this situation in several other ways — and sometimes the best move isn't on any list.

Qualify for two mortgages, buy, then recast. If your income supports carrying both loans, you can buy your next home on a traditional mortgage, list your current home, and once it sells, make a large lump-sum payment to your new mortgage and request a recast — the lender re-amortizes the remaining balance at the lower amount, dropping your monthly payment without a full refinance. This is clean, avoids bridge loan costs, and works well for buyers with solid income.

The family backstop. I've had buyers submit a cash offer — backed by funds from a family member — then list their current home. Once the current home was under contract, they converted to traditional financing. The seller got the certainty of a cash offer; the buyer got the house without a contingency; the family member's money was only briefly at risk. It requires trust and coordination, but when the pieces are in place, it's one of the smoothest paths I've seen.

The bottom line: there are more paths than most buyers realize. If you're feeling stuck between "I can't buy until I sell" and "I can't sell until I have somewhere to go," the answer usually involves a creative combination — not a single perfect product.

My Honest Starting Point

When a move-up buyer calls me and says they need to buy before they sell, the first thing I ask isn't about rates. I ask whether they can qualify for two mortgages at the same time. If the answer is yes, that opens up the widest range of options and the least expensive path. If the answer is no, we look at what equity they have, whether a bridge product makes sense, and whether their target home is the kind of listing where a contingency has a realistic shot.

I also ask whether they have a family member or financial backstop they'd be comfortable using temporarily. Not everyone does — and that's fine — but when they do, it often opens the door to a cleaner offer strategy that doesn't require a financing product at all.

Want to know what your current home is worth before you start planning? Get a free home evaluation here — knowing your equity is step one of every one of these conversations. And if you want to run the numbers on carrying two payments, the mortgage calculator on this site is a good place to start.

The buy-sell timing puzzle doesn't have to feel paralyzing. Most clients I work with find a workable path once we sit down and look at the whole picture — their equity, their income, their target price range, and what the market looks like on the sell side. If you're trying to figure out your move, let's talk.

Trying to Time Your Move? Let's Talk.

I'm Chris Jamison with Nebraska Realty, and buying before you sell is one of the most common puzzles I help move-up buyers solve across the Omaha metro. I'll look at your equity, your income, and your target price range, then help you find the path that actually fits your situation — bridge, HELOC, contingent offer, or something more creative. No pressure, just real guidance.

Let's Talk →Can I get a bridge loan if my current home isn't listed yet?

Yes, in most cases. Lenders like ACCESSbank and NBC Bank will typically fund a bridge loan before you've listed, as long as you can demonstrate sufficient equity and a clear plan to sell. You'll need to be realistic: the clock starts ticking on the loan term at closing, so you want your current home listed and priced correctly as quickly as possible after you close on the new purchase.

Will a HELOC lender freeze my line once I list my home?

It depends on the lender, but many will — or at minimum, they'll be restricted from letting you draw new funds once the collateral property is actively for sale. If you're planning to use a HELOC for a purchase, get the draw done before you list. Talk to your lender explicitly about this scenario before you count on those funds.

How long does a contingent offer usually stay active in Omaha?

The contingency period is negotiated in the contract — commonly 30 to 60 days. If the seller includes a kick-out clause (which is common), they can continue showing the home and give you a notice period — usually 48 to 72 hours — to either remove the contingency or release the contract. Understanding this going in helps you avoid surprises.

What's the cheapest way to buy before I sell?

If you can qualify for two mortgages, that's almost always the most cost-effective path — you're paying a market rate on both loans rather than the premium rate of a bridge product. If you can't qualify for two, a contingent offer (when a seller will accept it) is the next least expensive option because there's no additional financing cost at all. Bridge loans and HELOCs both carry costs; they're tools for situations where the other options aren't available.

Recent Posts